{kind=link}

Countries with weapons industries already working at full tilt have picked up a lot of early defense contracts.

This text is made up of selected passages from the article signed by Joshua Posaner, Lucia Mackenzie and Jan Cienski published in POLITICO on the 4th of December 2023

The West has pledged to do whatever it takes to support Ukraine while also returning militaries to a war-ready status, but it is defense contractors in South Korea, Turkey and Israel which are reaping many of the early deals.

Arms makers in those countries, where governments sustain military investment and production pipelines to maintain their own security, made early gains in the months following the February 2022 full-scale invasion of Ukraine by Russia, according to the latest analysis of weapon sales and military services revenue from the world’s top 100 contractors carried out by the Stockholm International Peace Research Institute (SIPRI).

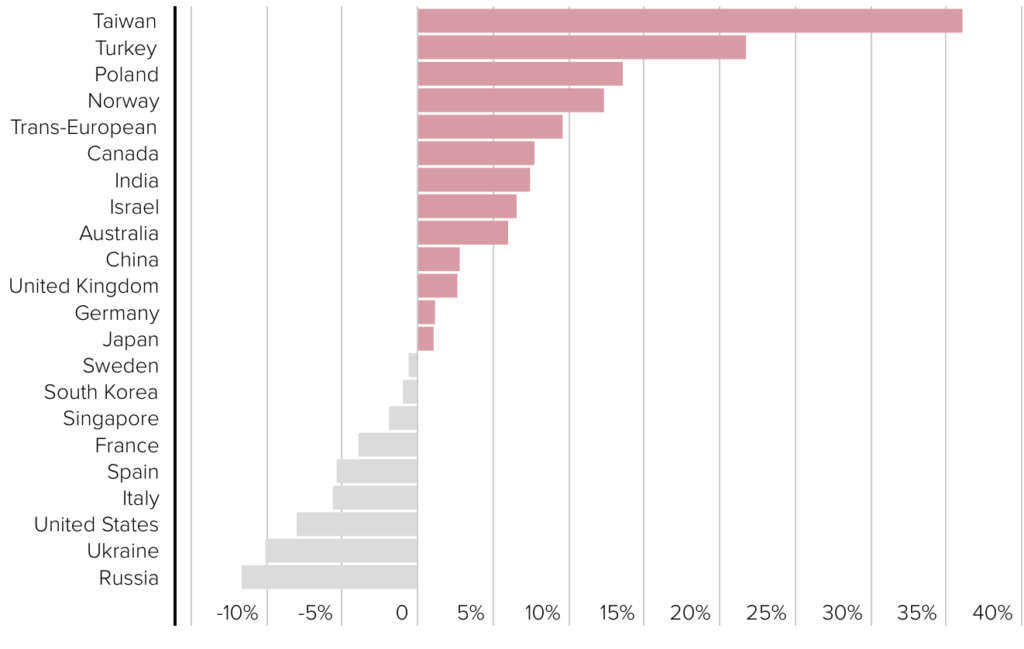

2022’S WINNERS AND LOSERS

While the analysis is from the immediate months after the start of the war, not all the contract revenue has yet trickled down to order books.

But, in contrast to major players in the United States and Europe which saw their revenues stall last year, contractors in a small group of countries are clearly on the up, judging by the percentage change in their arms revenue* from 2021 to 2022.

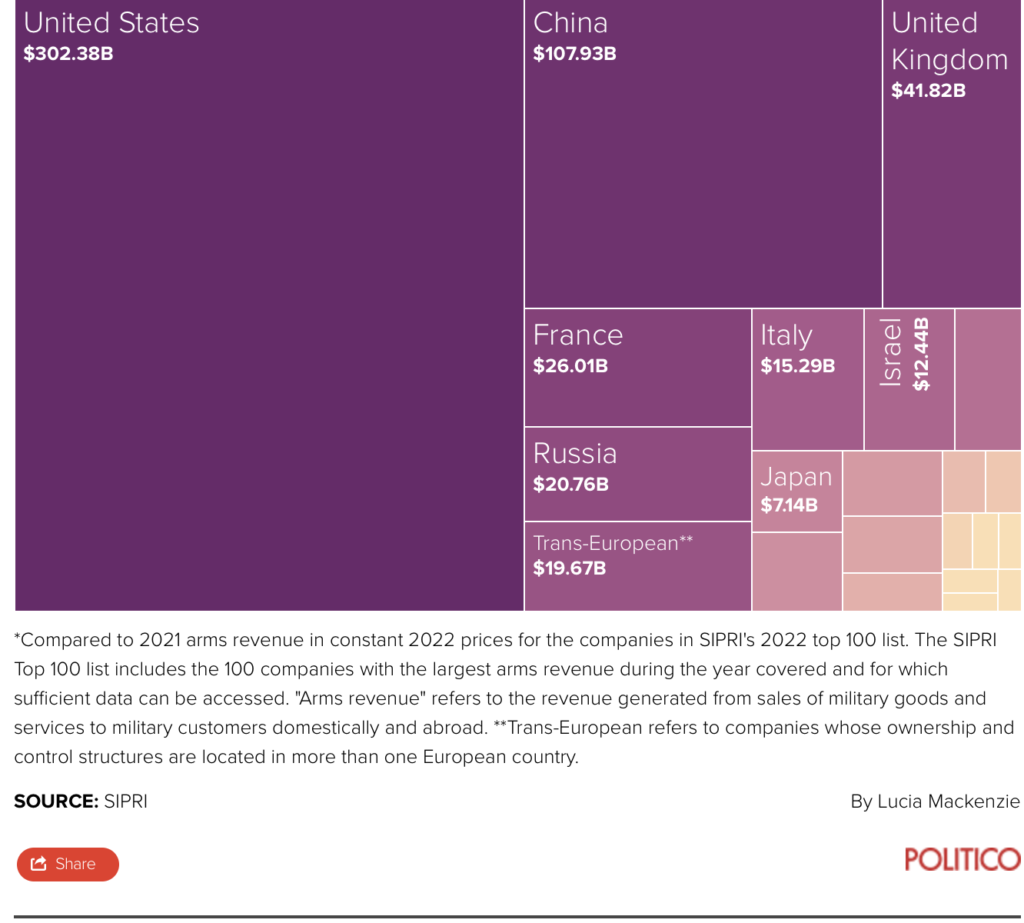

Despite a drop in the total arms revenue of American companies that are part of SIPRI’s top 100 list, these U.S. based companies remain dominant, with the largest combined arms revenue of $302 billion.

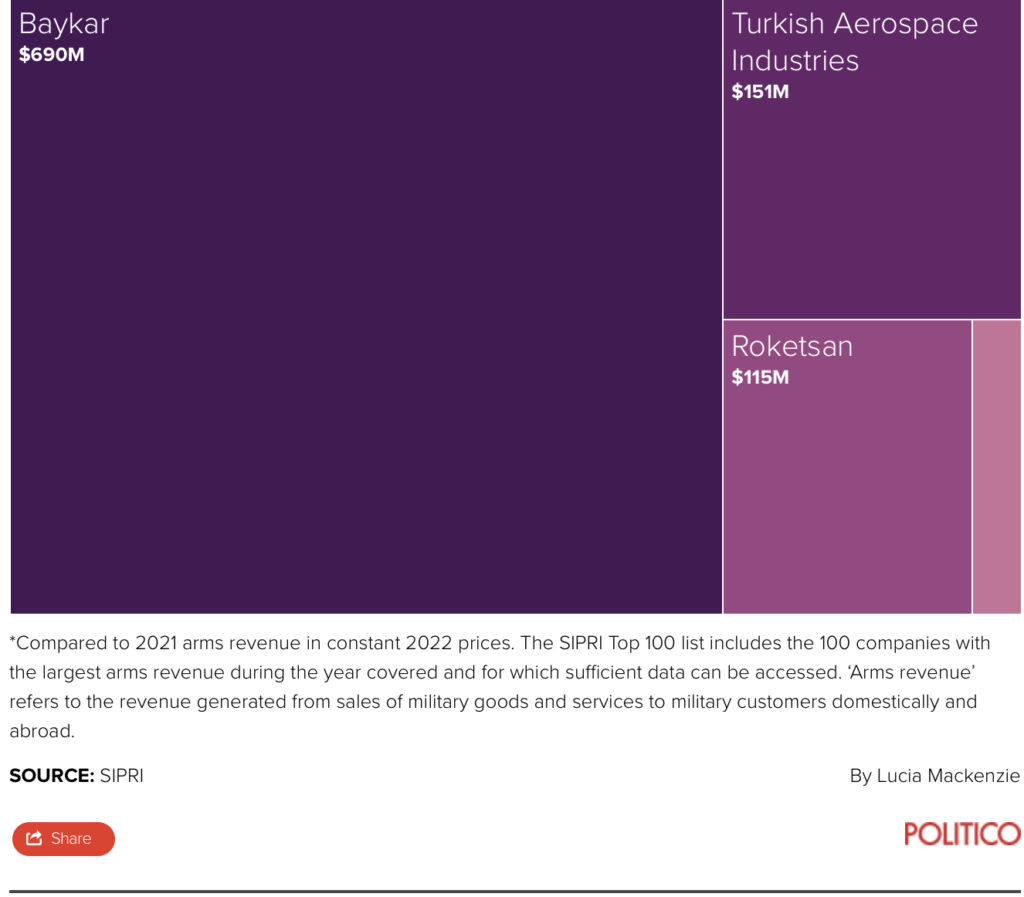

“South Korea, Israel, Turkey are countries that stand out as being able to respond to the increased expenditure,” said Lucie Béraud-Sudreau, who helped compile the data for SIPRI as part of an annual update that’s been ongoing since the end of the Cold War.Turkey’s four largest defense companies saw their 2022 revenues rise by 22 percent to $5.5 billion compared to 2021, with the standout being drone-maker Baykar.

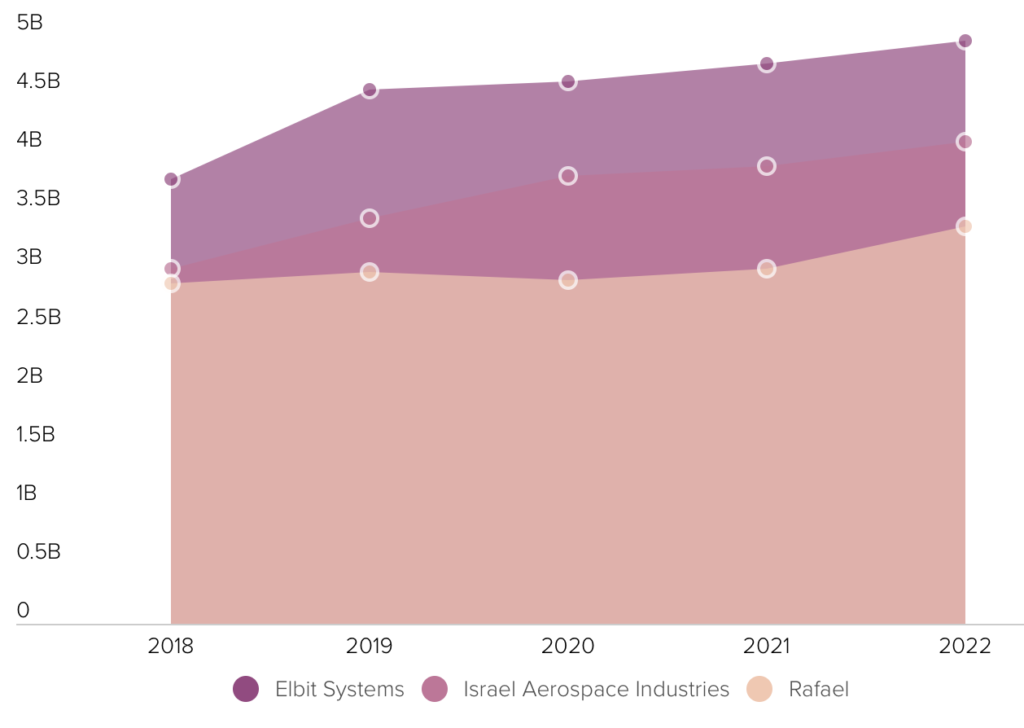

The aggregate arms revenues of the three Israeli companies in the SIPRI ranking reached $12.4 billion in 2022, a 6.5 percent increase compared with 2021.

The combined arms revenues of the four South Korean companies in the ranking fell by 0.9 percent, primarily due to an 8.5 percent drop recorded by the country’s biggest arms producer, Hanwha Aerospace; but South Korean companies are likely to see a surge in revenues this year due to huge orders with Poland and the United Arab Emirates.

Poland, a frontier state with Ukraine, has lodged massive orders with South Korean arms producers for K2 Black Panther tanks, K9 self-propelled howitzers and FA-50 fighter planes (not all of which are yet visible in SIPRI’s 2022 data, but should factor in this year). Warsaw traditionally looked to the U.S. for its big arms deals, but turned to South Korea because it was able to fill orders faster than backlogged U.S. companies.

In a signing ceremony last year, Polish Defense Minister Mariusz Błaszczak explained that “unfortunately due to limited industrial capabilities, it will not be possible for the equipment to be delivered in a satisfactory timeframe. Therefore, we started talks with South Korea — our proven partner.”

SPOTLIGHT ON ISRAEL AND TURKEY

Israel’s big three firms — Rafael, Israel Aerospace Industries and Elbit Systems — all saw increased arms revenue in 2022 compared to the previous year,* according to SIPRI.

Other producers have found their niche too. For example, Turkey’s Baykar, maker of the Bayraktar TB-2 drone used by Ukrainian forces, saw its revenue increase by 94 percent from 2021* to 2022 propelling the company into SIPRI’s top 100 list for the first time.

Baykar’s increase in arms revenue by $690M* dwarfs the gains made by other Turkish companies in the top 100 list.

The three countries are swinging into an early lead because their arms factories are already on war-ready footings.“Those are countries in a specific context that need their industries to be reactive,” said Béraud-Sudreau. “Also they are producing the stuff that’s in demand like artillery, drones.”

While U.S.-based titans Lockheed Martin, Raytheon and Boeing remain at the top of SIPRI’s list, arms revenues for all three declined in 2022, while the figures for Northrup and U.K.-based BAE Systems only slightly increased.

The arms revenues of the 42 largest U.S. defense companies fell by 7.9 percent to $302 billion in 2022.

« We are beginning to see an influx of new orders linked to the war in Ukraine and some major U.S. companies, including Lockheed Martin and Raytheon Technologies, received new orders as a result, » said Nan Tian, a SIPRI senior researcher. « However, because of these companies’ existing order backlogs and difficulties in ramping up production capacity, the revenue from these orders will probably only be reflected in company accounts in two to three years’ time. »

Meanwhile, in Europe, the likes of MBDA and Leonardo also saw arms revenue declines last year.

« Many arms companies faced obstacles in adjusting to production for high-intensity warfare, » said Béraud-Sudreau. « However, new contracts were signed, notably for ammunition, which could be expected to translate into higher revenue in 2023 and beyond. »

She added that weapons makers in the U.S. and Europe did receive a lot of new orders, but were unable to significantly ramp up production capacity because of labor shortages, soaring costs and supply chain difficulties.

The EU is currently in the midst of an intense debate over how to boost its defense production, and how to ensure that both national and European Union funds go to domestic companies rather than to foreign suppliers.

“Poland buys from South Korea, Estonia buys from Turkey, and we are not able to really have European products for our armed forces,” said Riho Terras, an Estonian MEP from the European People’s Party who was commander of the national army until 2018.

“That is something that we need to focus on, otherwise we will lose the competition against, especially, South Korea,” he told POLITICO earlier this year.

While the revenues of U.S. and European arms companies stuttered due to the transition to wartime production aimed at both supplying Ukraine and also building up national stocks, the big loser was Russia, whose defense companies have seen their revenues shrivel.

The Kremlin is not very forthcoming about defense sector data, so SIPRI only has two Russian companies in its ranking, but their combined arms revenues fell by 12 percent to $20.8 billion.

Béraud-Sudreau said the best guess is that Russian arms makers are still signing massive contracts to supply the Kremlin’s war effort, but that government payments are deferred so contractors are instead drawing on bank loans to cover costs.