{kind=link}

Turkey’s central bank is expected to leave interest rates at 45% on Thursday, but with inflation thrashing towards 70% again and the lira crashing another 9% this year, there is certainly an argument for another hefty hike.

Reuters, March 21, 2024, by Marc Jones, Canan Sevgili and Jonathan Spicer

Timing is everything though and with just over a week until nationwide local elections, where President Tayyip Erdogan’s AK Party is trying to win back key cities like Istanbul, the new central bank governor might have his work cut out.

Here are five key questions ahead of Thursday’s rate-setting meeting and the March 31 elections.

1/ HIKE OR HOLD?

With inflation expected to soon reach 70% most economists expect another rate hike this week, right? Well, not according to the latest Reuters poll where all but two of the 22 that participated predicted no change – though most expect some more monetary tightening in coming months.

The central bank has jacked up its key rate from 8.5% in June and Finance Minister Mehmet Simsek has reiterated inflation will be brought down with the help of tighter fiscal policy.

But Rajeeb Pramanik, at research firm BCA, says the main reason Turkey is still far from any kind of « macro-orthodoxy » is its continued fiscal largesse.

Fiscal stimulus cooled significantly after last year’s May general elections but picked up a bit in recent months ahead of the March vote.

Daron Acemoglu, a prominent Turkish-born professor at the Massachusetts Institute of Technology, also believes that the central bank’s inflation forecasts remain « unrealistic ».

With 67% inflation last month, « real » interest rates – central bank rates minus Turkey’s inflation rate – remain among the most negative in the world.

« If (rate hikes) still take you to negative real interest rates, that’s not going to be sufficient, » Acemoglu said.

2/ HOW DO YOU SOLVE A PROBLEM LIKE THE LIRA?

The crux of Turkey’s inflation problem remains the lira.

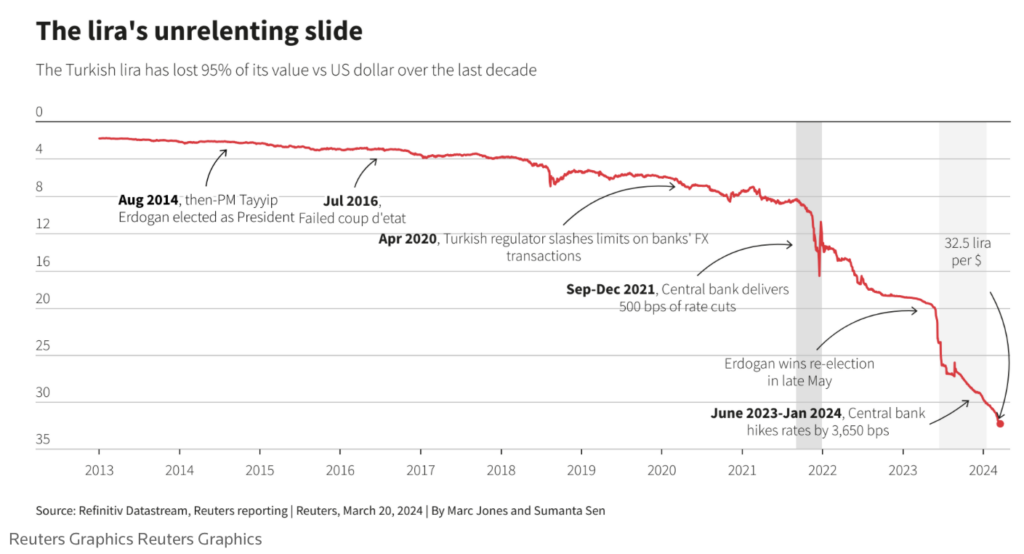

Turks have watched it lose over 95% against the U.S. dollar over the last decade, including 40% since last year’s elections and 9% since the start of 2024.

Reserves have been dropping again lately as well, although the Treasury has had no problem topping up in the debt markets.

Official figures show that net reserves excluding swaps decreased by approximately $6 billion last week, dipping to negative $60 billion.

ALB Chief Economist Filiz Eryılmaz said there could be « significant pressure » after the elections too if Turks continue to stash dollars, although that isn’t her base case.

3/ HOW ELSE IS THE BANK TIGHTENING CREDIT?

While the central bank has had its most aggressive run of rate hikes in decades – and promised to do more if it expects a « significant and persistent » deterioration in the inflation outlook – some things are not going exactly as planned.

Not only was inflation hotter than expected last month and reserves are leaking again, but surveys also suggest Turks see little relief ahead, casting some doubt on the central bank’s 36% year-end inflation forecast.

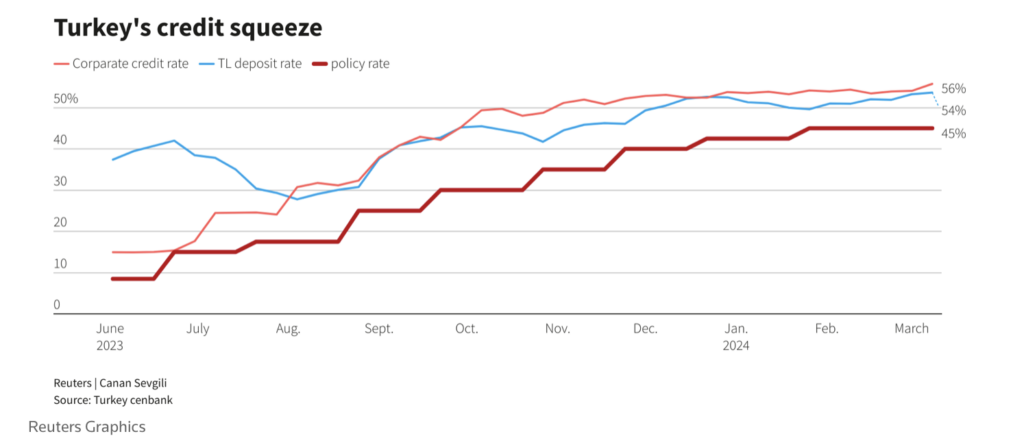

The bank has pulled various levers to tighten liquidity in the banking system: it imposed a block on portions of lenders’ lira required reserves; reduced the limits of installments on cash advances; raised the maximum rate on credit card cash withdrawals; and met privately with bank chiefs to press for tighter credit.

Some lenders have responded by cutting lira commercial loan limits, pushing up related rates to 60% – from below 15% before the May general elections. Lira deposit rates have risen to 54% from below 30% in August, though many savers still prefer dollars and euros.

4/ COULD ELECTIONS BRING ANOTHER POLICY SHIFT?

Turkey’s economic policy morphed after last year’s elections in which Tayyip Erdogan was re-elected president.

He promptly appointed a new cabinet and central bank leadership that pivoted away from years of unorthodoxy – which the president had long endorsed – back to a stance centred on hiking rates and freeing up forex and credit markets.

Recalling this 180-degree pivot, as well as years of rotating economic leadership, some investors are wondering what happens this time around.

« We deemed it prudent to buy some protection (on Turkish bond positions) ahead of the election, » said Giulia Pellegrini at Allianz Global Investors.

« There has been a lot of improvement, » she said. But it now becomes « more difficult in the management (and) you do have the risk of Erdogan interfering again in monetary policy, which we learned over the years is never far off. »

Yet fiscal stimulus has been muted ahead of the vote. Even after former Central Bank Governor Hafize Gaye Erkan abruptly resigned in February, authorities stressed policy remained on track under former bank deputy and new chief Fatih Karahan.

ALB’s Eryilmaz said she expects the inflation fight to continue after the vote. « No risks can be taken anymore. The economic management is aware of this, » she said.

5/ DO YOU HAVE WHATEVER IT TAKES?

FX markets though are speculating that after the vote – for which Erdogan is campaigning hard for his party to re-take Istanbul and other cities from the opposition – rates could rise even higher alongside steps to tighten fiscal policy.

Kieran Curtis, a veteran Turkey investor at Abrdn, thinks it will only be clear how serious policymakers really are about beating inflation around the middle of the year when they must decide whether or not to raise wages again.

The government hiked the minimum wage by a larger-than-expected 49% in December and by 55% the year before.

« They have done some policy normalisation but that has slowed and FX has started to leave again, so it’s not a straight line improvement, » Curtis said. « So we need them to get back to work after the elections and keep the disinflation story alive. »